Chapter 15

Capital structure decisions Decisions about a firm’s debt-equity ratio à refers to

financial leverage

Capital restructurings Changes that also make the debt-equity ratio change

à these only benefit shareholders if and only if (!) the

market value of the firm increases

Which capital structure is the best: the one that maximizes the share’s value and thus

minimizes the WACC à managers will choose the capital structure that they think will have

the highest market value because this capital structure will be more beneficial to the firm’s

shareholders.

Target capital structure Optimal capital structure

Financial leverage Extend of the firm that relies on debt

Net income

EPS (earnings per share) =

# shares

𝑁𝑒𝑡 𝑖𝑛𝑐𝑜𝑚𝑒

𝑅𝑂𝐸 𝑟𝑒𝑡𝑢𝑟𝑛 𝑜𝑛 𝑒𝑞𝑢𝑖𝑡𝑦 =

𝑡𝑜𝑡𝑎𝑙 𝑒𝑞𝑢𝑖𝑡𝑦

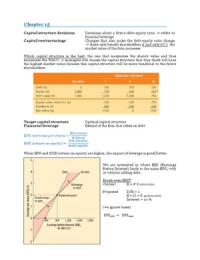

When EPS and ROE (return on equity) are higher, the impact of leverage is good/better.

We are interested in where EBI (Earnings

Before Interest) leads to the same EPS, with

or without adding debt.

Break-even EBIT

Current E = € 8.000.000

Proposed D/E = 1

E = D = € 4.000.000

Interest = 10 %

(we ignore taxes)

𝐸𝑃𝑆!"# = 𝐸𝑃𝑆!"#

,Based on autoveloce is stated that:

§ The effect of financial leverage depends on EBIT, when EBIT > BEP it is beneficial

§ In expected situation, leverage increases returns on shareholders (ROE and EPS)

§ Proposed situation gives more risks to shareholders (EPS and ROE are more

sensitive)

§ The capital structure is very important

Homemade leverage Use of personal borrowing to change overall amount of

financial leverage to which the individual or investor is

exposed (see also table 15.5 and example 15.2)

M & M: Modigliani and Miller

M&M I States that the value of the firm is independent f its capital structure (pie

model)

Key assumptions:

- No taxes

- No transaction costs

- Individual and corporate borrow at the same rate

M&M II States that the total value of the firm is not affected by the capital

structure, although debt and equity is (à cost equity and financial

leverage)

! !

WACC = 𝑥 𝑅𝑒 + 𝑥 𝑅𝑑

! !

V= E+D

!

Re = 𝑅𝑎 + 𝑅𝑎 − 𝑅𝑑 𝑥

!

The cost of equity (Re) depends on:

1. Required rate of return (Ra)

2. Cost of debt (Rd)

3. Debt-equity ratio (D/E)

See example 15.3

Business risk Equity risk that comes from nature of the operating activities à

in the formula; Ra

Financial risk Equity risk from the financial policies (capital structure) à by

using more debts à in formula; (Ra-Rd) X (D/E)

An all in equity firm, has a zero cost of equity!

There are 2 features of debt:

1. Interest paid over debt is tax deductible (positive)

2. Failure can mean direct bankruptcy (negative)

Interest tax shield Tax savings by a firm from the interest expense (see example

given on page 455).

𝑇! ×𝐷 ×𝑅!

𝑃𝑉 𝑜𝑓 𝑡𝑎𝑥 𝑠ℎ𝑖𝑒𝑙𝑑 = = 𝑇! ×𝐷

𝑅!

There are 2 different bankruptcy costs:

Direct Directly associated with bankruptcy (e.g. legal expenses)

Indirect Costs for avoiding bankruptcy

, Debt in a firm can cause conflicts of interests between shareholders and bondholders à most

of the time the shareholders go selfish, there are 3 different ‘selfish’ strategies for that:

1. Incentive to take large risks (high risks, low or negative NPV)

2. Incentive towards under investments (not investing in existing positive NPV projects)

3. Milking the property (pay out extra dividends or other distributions in times of

financial distress)

Static theory of A firm borrows to a point where tax benefit equals cost from

capital structure increased probability of financial distress (see figure 15.6)

The difference between the static value and the actual value is the loss in value from the

probability of financial distress.

In real life, most large firms use little debt à this is in contrary of what M&M states! à

Pecking-order theory Use of internal financing when possible, for example: selling

securities is expensive. But also, insiders have more information

about the firm!

1. Internal financing

2. Debt financing

3. Equity financing

Signaling theory Increasing debt levels signals firms expected higher profitability,

this is has a positive effect on a firm’s value à can be used to fool

investors

Implication in the pecking-order theory:

§ There’s no target capital structure

§ Profitable firms use less debt

§ Companies will want financial slack

Types of bankruptcy:

1. Business failure

2. Legal bankruptcy

3. Technical insolvency

4. Accounting insolvency

The benefits of buying summaries with Stuvia:

Guaranteed quality through customer reviews

Stuvia customers have reviewed more than 700,000 summaries. This how you know that you are buying the best documents.

Quick and easy check-out

You can quickly pay through credit card or Stuvia-credit for the summaries. There is no membership needed.

Focus on what matters

Your fellow students write the study notes themselves, which is why the documents are always reliable and up-to-date. This ensures you quickly get to the core!

Frequently asked questions

What do I get when I buy this document?

You get a PDF, available immediately after your purchase. The purchased document is accessible anytime, anywhere and indefinitely through your profile.

Satisfaction guarantee: how does it work?

Our satisfaction guarantee ensures that you always find a study document that suits you well. You fill out a form, and our customer service team takes care of the rest.

Who am I buying these notes from?

Stuvia is a marketplace, so you are not buying this document from us, but from seller s1305492. Stuvia facilitates payment to the seller.

Will I be stuck with a subscription?

No, you only buy these notes for $3.72. You're not tied to anything after your purchase.