Samenvatting van Advanced Corporate Financial Management van alle colleges, collegesheets en deel van de literatuur. Docent: H. Rijken. Opleiding: Master Business Administration - Financial Management.

Summary of Advanced Corporate Financial Management.

Long-term financing, corporate capital structure

- If a business is not healty you can’t fix it with finance solutions. The business

itself has to be oke, and in that case it is possible to gain more advantages with

finance solutions.

Financing risk: - solvancy E/D ratio = Long-term risk KE (= cost of equity)

- Net working capital (NWC) = Short-term risk KD (= cost of

debt)

* A company can’t have high risk of both. Usually they have one of them.

* Financing risk is the risk of the debtholder. Business risk is the risk of the equity

holder.

* KE + KD = WACC

Business risk = risk of the firm’s assets when no debt is used. It is inherent in the

company’s operations. Many factors (bv. Sales risk & input-cost risk) affect

business risk and the more volatile these factors are, the riskier the company is.

Business risk is market based.

Financial risk = takes in account a company’s leverage. High leverage = high

risk to stockholders, because the probability that they don’t get their money back

is high, because of more debt.

- Accounting based balance sheet is about the past.

Market based is about the future.

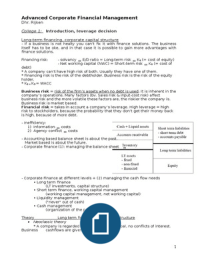

- Corporate finance (1): managing the balance sheet

- Corporate Finance at different levels + (2) managing the cash flow needs

• Long term finance

(LT investments, capital structure)

• Short term finance, working capital management

(working capital management, net working capital)

• Liquidity management

("never" out of cash)

• Cash management

(organization of the payments flow)

Theory Long term financing: the capital structure

Neoclassic theory

* A company is regarded as a black box. One goal, no conflicts of interest.

Business cashflows are given.

1

, * Perfect market: capital will flow to business opportunities with optimal risk-

return relationship.

No tax, no transaction costs, no information costs, no distress (market-

efficiency)

* Symmetric information (homogeneous perceptions and expectations) → no

agency costs

* Investors are risk-averse

→ Abstract framework to build financial models

Literatuur: - Chapter 2 (2.1-2.5) PDF file (niet alles letterlijk gelezen, formules

overgeslagen)

Valuation and Financing decisions in an ideal capital market

2.2 Defining an ideal capital market:

5 assumptions in ‘ideal capital market’:

1. Capital markets are frictionless (no taxes, transactions costs etc.)

2. All market participants share homogeneous expectations (information is free

available)

3. All market participants are atomistic (no one can affect the market

price)

4. The firm’s investment program is fixed and known to all investors

5. The firm’s financing is fixed

The purpose of studying theory under ideal conditions is twofold:

1. We gain insights into the effects of a firm’s decisions on the values and risk

of iets securities

2. Armed with an understanding of the effects of corporate financial decisions

under ideal conditions, we are in a better position to understand the

incremental effects (where the increment = vermeerdering smay be large)

of certain real-world factors (which constitute violations of one or more of

the ideal capital market assumptions) on both these decisions and their

effects.

2.4 The irrelevance of dividend policy

- If a firm’s captial investement and debt policy are fixed, then as the firm

increases its dividend, it will eventually have to finance such payments by issuing

shares. A dividend is actually a partial liquidation of the original shareholders’

interest in the firm. If a shareholder receives dividend he can restore his

proportional claim on the firm by purchasing some shares.

2.5The capital asset princing model

The Modern Portfolio Theory involves two basic constructs:

1. The statistical effects of diversification on the expected return and risk of a

portfolio

2. The attitudes of investors toward risk: they averse it, but they are tolerant of

risk to bear if it is sufficient compensated.

- Theory shows that around 30 numbers of securities is needed to gain an optimal

portfolio mix.

CAPM = A model that describes the relationship between risk and expected return

and that is used in the pricing of risky securities.

2.5.2 Market equilibrium (markt evenwicht): the capital market line (CML)

- CML = a line that is created by the choices available to investors in r – sigma

space, that is formed by the points representing the Rf security and M (=market

portfolio).

College 2: Leverage decision (1)

2

, Proposition Modigliani & Miller, MM1 Value

- In the neo-classic framework the company value is independent to the

financing decision. Only the asset value determines the value of a company.

Proposition Modigliani & Miller, MM2 Cost of capital

- In the neo-classic framework the total costs of capital are independent to the

financing decision.

WACC = gelijk aan Re bij 100% Equity. Ke = Business risk + financing risk * D/E

Assumptions:

1. Strict separation between business (assets) and financing decision (liabilities)

2. Always financing available, given the business cash flows.

Definitions cost of capital in a MM world with corporate taxation

- With tax the finance decision does impact the value of the company.

- WACC = Kvv•(1-T)•(D/TV) +Kev•(E/TV) (definition)

- WACC = ρ _[ 1 - T•(D/TV) ] (derived)

- TV = E + D ( = market value E + market value D)

- Vu = CFu/market risk

- Vl = Cfu/market risk + (Kb*B/Kd)

“anomaly”: Income Tax (MM + all tax)

- T1 = extra tax rate, in this case for example income tax.

“view I”: Insolvency costs (Static Trade off theory)

- The risk of bankruptcy/default.

- Insolvency costs show up in:

1a) Direct costs (settlement costs, loss of tax credit due to net operating

losses)

= P(bankruptcy) x (costs settlement + tax credit)

1b) Indirect costs. Are far more important:

* suppliers / clients are less willing to do business (the strict separation

between business and financing disappears)

* conflict of interest between shareholders (option value) and

bondholders / banks (timing bankruptcy)

* bad reputation for investors etc. etc.

- 1a and 1b results in lower (expected) cash flows

1 2) an increase in business risk and financing risk, resulting in higher

financing costs, mostly an extra credit risk premium ( plus extra

equity risk premium)

- 1 and 2 results in turn to a lower company value (= insolvency costs)

- Wacc first goes down if D/E ratio is increasing, but at a certain point it will go up,

because of the higher risk of high debt.

“view II”: Agency costs

“view III”: Pecking order theory

- If you need cash you try to gain it in the following order:

3

, 1) Internal cash

2) Debt

3) Shares

4) Hybrid products

- A concept on leverage decision: Static Trade Off theory

Trade off between tax advantages and bankruptcy costs, so it’s about the

amount of leverage a company prefers.

Optimum is somewhere within an interval (given by business risk). There is

a target ratio.

- A concept on leverage decision: Pecking order theory

= Companies prioritize their sources of financing.

Complete different perspective on capital structure decisions

Information asymmetry between equity issuer and investor (managers know

more about the company than investors

Does not seek for an optimal capital structure. There is no target ratio.

- No difference in characteristics between Static Trade off and Pecking Order firms

- MM theory is the base. From there we add all kind of things that contradict the

assumptions of a perfect market. (taxes, insolvency costs, agency costs, etc..)

- The financing risk can influence the business risk. Because a companies relations

want continue business. They don’t want that one company out of the

‘productionline’ goes bankrupt.

Overview concepts on capital structure (toolbox)

- Bottom line: Asset Risk versus Financing Risk

Asset Risk and Financing Risk must be somewhat balanced in such a way

that insolvency costs are at a reasonable/acceptable level for most

investors.

A “first order” estimate of what a firms capital structure should be is

determined by

- Life cycle

- Size

- Sector

Life cycle, size, sector are first order indicators of asset risk

- a mature company has on average 60% debt. A start up has 100% equity and a

growth/innovative company 80-90% equity.

Target capital structure is strongly related to the sector (business characteristics)

1 Trade Industry Con Service

- (example) proxies for business risk

2 * Salary costs / sales - +/- +/- ++

- fixed / variable costs

1 * Profit - +/- - +

- cash flow level

- (example) proxies for financing risk

1 * Collateral ++ + +/- -

2 * Target capital structure 25% 45% 30% 30%

- Each industry has different leverage intervals. (bv. Finanical services 85-70% &

retail 30-10%)

Views / concepts on capital structure decisions

Bottom line (large picture)

- Balance between business risk and financing risk (insolvency costs)

Academic concepts

- Static Trade off theory

- Pecking Order Theory

4

The benefits of buying summaries with Stuvia:

Guaranteed quality through customer reviews

Stuvia customers have reviewed more than 700,000 summaries. This how you know that you are buying the best documents.

Quick and easy check-out

You can quickly pay through credit card or Stuvia-credit for the summaries. There is no membership needed.

Focus on what matters

Your fellow students write the study notes themselves, which is why the documents are always reliable and up-to-date. This ensures you quickly get to the core!

Frequently asked questions

What do I get when I buy this document?

You get a PDF, available immediately after your purchase. The purchased document is accessible anytime, anywhere and indefinitely through your profile.

Satisfaction guarantee: how does it work?

Our satisfaction guarantee ensures that you always find a study document that suits you well. You fill out a form, and our customer service team takes care of the rest.

Who am I buying these notes from?

Stuvia is a marketplace, so you are not buying this document from us, but from seller BtB12. Stuvia facilitates payment to the seller.

Will I be stuck with a subscription?

No, you only buy these notes for $4.82. You're not tied to anything after your purchase.