Week 3 :

Preparation: Chap 6: Production

Production decision of a firm can be understood in 3 steps (refers to the theory of the

firm-> Explanation of how a firm makes cost-minimizing production decisions and

how its cost varies with its output):

- Productions technology: we need a practical way of describing how inputs can

become outputs.

- Cost constraints: Taking into account of the price of labor, capital, and other

inputs.

- Input choices: given its production technology and the prices of labor, capital

and other inputs, the firm must choose how much of each input to use.

Factors of production: inputs into the production process.

A production function is showing the highest output that a firm can produce for every

specified combination of inputs.

Inputs and outputs are flows. Production functions describe what is technically

feasible when the firm operates efficiently.

Short run is a period of time in which quantities of one or more production factors

cannot be changed.

Fixed input is a production factor that cannot be varied.

The long run is the amount of time needed to make all production inputs variable.

Average product is an output per unit of a particular input. = q/L

Marginal product is an additional output produced as an input is increased by one

unit. =∆q/∆L

When the marginal product is greater than the average product, the average product

is increasing. When the marginal product is less than the average product, the

average product is decreasing.

In general, the average product of labor is given by the slope of the line drawn from

the origin to the corresponding point on the total product curve.

In general, the marginal product of labor at a point is given by the slope of the total

product at that point.

The law of diminishing marginal returns is the principle that as the use of an input

increases with other inputs fixed, the resulting additions to output will eventually

decrease. Describe a declining marginal product but not necessarily a negative one.

Labor productivity: Average product of labor for an entire industry or for the economy

as a whole. Determines the real standard of living achieving by a country for its

citizens.

Stock of capital: Total amount of capital available for use in production.

Technological change is the development of new technologies allowing factors of

production to be used more effectively.

Isoquant is curve showing all possible combinations of inputs that yield the same

output. A graph combining a number of isoquants is called an isoquant map, used to

describe a production function.

MRTS (Marginal Rate of Technical Substitution) is the slope of the isoquants. It is the

amount by which the quantity of one input can be reduced when one extra unit of

another input is used, so that output remains constant. Analogous to the MRS in

consumer theory.

MRTS= - Change in Capital input / change in labor input

, MRTS= -∆K / ∆L (fixed lvl of q)

Diminishing: we assume that it’s diminishing (MRTS falls as we move down along the

isoquant.

Additional output from increased use of labor = (MPL)(∆L)

Reduction in output from decreased use of capital = (MP K)(∆K).

So because output are hold constant by moving along an isoquant, (MP L)(∆L) + (MPK)

(∆K) = 0

(MPL) / (MPK) = -(∆K/∆L) = MRTS -> The MRTS btw 2 inputs = the ratio of the

marginal products of the inputs.

Fixed-proportions production functions (Leontief production function) has L-shaped

isoquants, so that the only one combination of labor and capital can be used to

produce each level of output.

Returns to scale: rate at which output increases as inputs are increased

proportionately.

Increasing returns to scale: situation in which output more than doubles when all

inputs are doubled.

Constant returns to scale is a situation in which output doubles when all inputs are

doubled.

Decreasing returns to scale is a situation in which output less than doubles when all

inputs are doubled.

The greater the return to scale, the larger the firms in an industry.

Chap 7: Cost of

production

Optimal combination of inputs: cost-minimizing.

Accounting cost are actual expenses + depreciation charges for capital equipment ->

the cost that financial accountant measures.

Economic costs are costs to a firm of utilizing economic resources in production. ->

Economists concern.

Opportunity cost is associated with opportunities forgone when a firm’s resources are

not put to their best alternative use (economic cost of doing business)

Sunk cost ≠ opportunity cost: expenditure that has been made and cannot be

recovered. (should always be ignored in making future economic decisions -> Its

opportunity cost is zero). Prospective sunk cost is an investment when the firm must

decide whever it’s economical (‘ll lead to a flow of revenues large enough to justify

its cost).

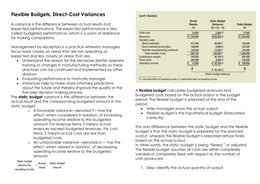

Total cost (TC or C) is the total economic cost of production, consisting of fixed and

variable costs.

Fixed cost (FC) does not vary with the level of output and that can be eliminated only

by shutting down. (≠ Sunk costs)

Variable cost (VC) varies as output varies.

Shutting down’s not necessarily going out of business, can be just selling what’s

already produced without using electricity etc …

Variable or fixed depend mainly on the time basis (the longer the more variable

costs).

Amortization is the policy of treating a one-time expenditure as an annual cost

spread out over some number of years.

Marginal Cost (MC) also called incremental cost, is an increase in cost resulting from

the production of one extra unit of output. MC = ∆VC / ∆q = ∆TC / ∆q

Preparation: Chap 6: Production

Production decision of a firm can be understood in 3 steps (refers to the theory of the

firm-> Explanation of how a firm makes cost-minimizing production decisions and

how its cost varies with its output):

- Productions technology: we need a practical way of describing how inputs can

become outputs.

- Cost constraints: Taking into account of the price of labor, capital, and other

inputs.

- Input choices: given its production technology and the prices of labor, capital

and other inputs, the firm must choose how much of each input to use.

Factors of production: inputs into the production process.

A production function is showing the highest output that a firm can produce for every

specified combination of inputs.

Inputs and outputs are flows. Production functions describe what is technically

feasible when the firm operates efficiently.

Short run is a period of time in which quantities of one or more production factors

cannot be changed.

Fixed input is a production factor that cannot be varied.

The long run is the amount of time needed to make all production inputs variable.

Average product is an output per unit of a particular input. = q/L

Marginal product is an additional output produced as an input is increased by one

unit. =∆q/∆L

When the marginal product is greater than the average product, the average product

is increasing. When the marginal product is less than the average product, the

average product is decreasing.

In general, the average product of labor is given by the slope of the line drawn from

the origin to the corresponding point on the total product curve.

In general, the marginal product of labor at a point is given by the slope of the total

product at that point.

The law of diminishing marginal returns is the principle that as the use of an input

increases with other inputs fixed, the resulting additions to output will eventually

decrease. Describe a declining marginal product but not necessarily a negative one.

Labor productivity: Average product of labor for an entire industry or for the economy

as a whole. Determines the real standard of living achieving by a country for its

citizens.

Stock of capital: Total amount of capital available for use in production.

Technological change is the development of new technologies allowing factors of

production to be used more effectively.

Isoquant is curve showing all possible combinations of inputs that yield the same

output. A graph combining a number of isoquants is called an isoquant map, used to

describe a production function.

MRTS (Marginal Rate of Technical Substitution) is the slope of the isoquants. It is the

amount by which the quantity of one input can be reduced when one extra unit of

another input is used, so that output remains constant. Analogous to the MRS in

consumer theory.

MRTS= - Change in Capital input / change in labor input

, MRTS= -∆K / ∆L (fixed lvl of q)

Diminishing: we assume that it’s diminishing (MRTS falls as we move down along the

isoquant.

Additional output from increased use of labor = (MPL)(∆L)

Reduction in output from decreased use of capital = (MP K)(∆K).

So because output are hold constant by moving along an isoquant, (MP L)(∆L) + (MPK)

(∆K) = 0

(MPL) / (MPK) = -(∆K/∆L) = MRTS -> The MRTS btw 2 inputs = the ratio of the

marginal products of the inputs.

Fixed-proportions production functions (Leontief production function) has L-shaped

isoquants, so that the only one combination of labor and capital can be used to

produce each level of output.

Returns to scale: rate at which output increases as inputs are increased

proportionately.

Increasing returns to scale: situation in which output more than doubles when all

inputs are doubled.

Constant returns to scale is a situation in which output doubles when all inputs are

doubled.

Decreasing returns to scale is a situation in which output less than doubles when all

inputs are doubled.

The greater the return to scale, the larger the firms in an industry.

Chap 7: Cost of

production

Optimal combination of inputs: cost-minimizing.

Accounting cost are actual expenses + depreciation charges for capital equipment ->

the cost that financial accountant measures.

Economic costs are costs to a firm of utilizing economic resources in production. ->

Economists concern.

Opportunity cost is associated with opportunities forgone when a firm’s resources are

not put to their best alternative use (economic cost of doing business)

Sunk cost ≠ opportunity cost: expenditure that has been made and cannot be

recovered. (should always be ignored in making future economic decisions -> Its

opportunity cost is zero). Prospective sunk cost is an investment when the firm must

decide whever it’s economical (‘ll lead to a flow of revenues large enough to justify

its cost).

Total cost (TC or C) is the total economic cost of production, consisting of fixed and

variable costs.

Fixed cost (FC) does not vary with the level of output and that can be eliminated only

by shutting down. (≠ Sunk costs)

Variable cost (VC) varies as output varies.

Shutting down’s not necessarily going out of business, can be just selling what’s

already produced without using electricity etc …

Variable or fixed depend mainly on the time basis (the longer the more variable

costs).

Amortization is the policy of treating a one-time expenditure as an annual cost

spread out over some number of years.

Marginal Cost (MC) also called incremental cost, is an increase in cost resulting from

the production of one extra unit of output. MC = ∆VC / ∆q = ∆TC / ∆q