Allocation of Support-Department Costs, Single-Rate and Dual-Rate Methods

Common Costs and Revenue

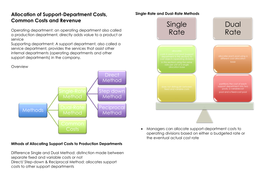

Single Dual

Operating department: an operating department also called

a production department, directly adds value to a product or Rate Rate

service

Supporting department: A support department, also called a

service department, provides the services that assist other

allocates

internal departments (operating departments and other costs in each cost pool (support

allocates each pool using a

support departments) in the company. department in this section) to

cost objects (operating divisions different cost-allocation

in this section) using the same base

rate per unit of a single

Overview allocation base

Direct

Method

partitions the cost of each

does not distinguish between support department into two

fixed and variable costs pools, a variablecost

Single-Rate Step down pool and a fixed-cost pool

Method Method

Dual-Rate Peciprocal

Methods

Method Method

Common

Costs Managers can allocate support-department costs to

operating divisions based on either a budgeted rate or

the eventual actual cost rate

Mthods of Allocating Support Costs to Production Departments

Difference Single and Dual Method: distinction made between

separate fixed and variable costs or not

Direct/ Step-down & Reciprocal Method: allocates support

costs to other support departments

Common Costs and Revenue

Single Dual

Operating department: an operating department also called

a production department, directly adds value to a product or Rate Rate

service

Supporting department: A support department, also called a

service department, provides the services that assist other

allocates

internal departments (operating departments and other costs in each cost pool (support

allocates each pool using a

support departments) in the company. department in this section) to

cost objects (operating divisions different cost-allocation

in this section) using the same base

rate per unit of a single

Overview allocation base

Direct

Method

partitions the cost of each

does not distinguish between support department into two

fixed and variable costs pools, a variablecost

Single-Rate Step down pool and a fixed-cost pool

Method Method

Dual-Rate Peciprocal

Methods

Method Method

Common

Costs Managers can allocate support-department costs to

operating divisions based on either a budgeted rate or

the eventual actual cost rate

Mthods of Allocating Support Costs to Production Departments

Difference Single and Dual Method: distinction made between

separate fixed and variable costs or not

Direct/ Step-down & Reciprocal Method: allocates support

costs to other support departments