Summary of FM2 including a recap on FM1, CH 5, 13, 8, 3, 6, 12. Clear summary with everything included. examples, theory, figures, explanations, pictures, etc.

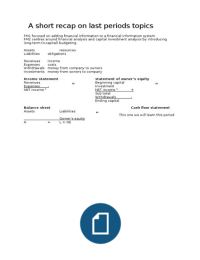

A short recap on last periods topics

FM1 focused on adding financial information to a financial information system

FM2 centres around financial analysis and capital investment analysis by introducing

long-term (=capital) budgeting.

Assets resources

Liabilities obligations

Revenues income

Expenses costs

Withdrawals money from company to owners

Investments money from owners to company

Income statement statement of owner’s equity

Revenues Beginning capital

Expenses - Investment

NET income 1 NET income 1 +

Sub total

Withdrawals -

Ending capital

Balance sheet Cash flow statement

Assets Liabilities

This one we will learn this period

Owner’s equity

A = L + OE

,Chapter 5 – Foundations of Financial

Reporting and the classified balance sheet

Financial reporting

Profitability and liquidity are important measures for investors and creditors; financial

statements support these decision makers and should enable these users to do the

following:

1. asses cash flow prospects

2. assess stewardship

Aside from financial statements, financial reporting also involves other information such

as management’s explanations, assumptions, uncertainties and estimates.

Familiarity with the accounting conventions enables the user to better understand

accounting information. Among these accounting conventions are:

- Consistency requires that once a company has adopted an accounting

procedure, it must use if from one period to the next

- Full disclosure requires that financial statements present all the information

relevant to users’ understanding

- Materiality refers to the relative importance of an item or event.

Conservatism applies when accountants have to choose between two equally

acceptable procedures: they should choose the one that is least likely to overstate assets

an income.

Cost-benefit holds that benefits to be gained from providing accounting information

should be greater than the cost of this information.

Under the Sarbanes-Oxley act, chief executive officers and chief financial officers of al

publicly traded companies must certify that, to their knowledge, their quarterly and

annual statements are accurate and complete.

Fraudulent financial reporting can have high costs for investors, lenders, employees and

customers as well as for the people who condone authorize or prepare misleading reports.

Reality does not change; numbers are only

represented differently.

Assets are divided into 4 categories. These are

listed in the order of how easily they can be

converted to cash.

- Current assets – include cash and other

assets that a company can reasonably

expect to convert to cash, sell or consumer

within one year of its normal operating

cycle, whichever is longer.

o A company’s normal operating

cycle is the average time it needs to

go from spending to receiving cash.

- Investments include assets, usually long-

term, that are not used in normal business

operations and that management does not

plan to convert to cash within the next year

- Property, plant and equipment include tangible long-term assets used in a

business’s day-to-day operations. (fixed assets)

- Intangible assets are long-term assets with no physical substance. Their value

stems from the right or privileges accruing to their owners

Liabilities are divided into 2 categories:

- Current liabilities – obligations that must be satisfied within one year or within

the company’s normal operating cycle, whichever is longer (notes payable,

accounts payable, salaries etc.)

- Long-term liabilities – debts that fall due more than one year in the future or

beyond the normal operating cycle (long-term notes, mortgages payable,

employee pension obligations)

Owner’s equity is the owner’s interest in a company. The equity section of the balance

sheet differs depending on whether the business is a sole proprietorship, a partnership of

a corporation:

- Sole proprietorship – this owner’s equity would just be the capital of the owner

in the company

- Partnership – the equity section of a partnership’s balance sheet is called

partner’s equity. It is both owner’s capital added up.

- Corporation – the equity section of a balance sheet for a corporation is called

stockholders’ equity. It has two parts:

o Contributed capital (paid-in capital) – reflects the amount of assets

invested by stockholders.

, o Retained earnings (earned capital) – represents the stockholders’ claim

to the assets that are earned from operations and reinvested in corporate

operations.

Dividends distributions of assets to shareholders.

Multi-step income statement

This income statement goes through a series of

steps to arrive at net income. It is for a service

company (which buys and sells products) than a

manufacturing company (which

makes and sells products).

NET sales = Gross sales – sales returns and allowances.

Gross sales – the total revenue from cash and credit sales during a period

Sales returns and allowances – cash refunds and credits on account. (also include

discounts).

Cost of goods sold is the amount a merchandiser paid for the merchandise it sold

during a period.

Gross margin = NET sales – cost of goods sold

Managers are interested in both the amount and percentage of gross margin

% gross margin = gross margin / NET sales

operating expenses are the expenses, other than the cost of goods sold, that are

incurred in running a business. They are often grouped into the categories of selling

expenses and general and administrative expenses.

Operating expenses = selling expenses + general and administrative expenses

Selling expenses – include the costs of storing goods and preparing them for sale;

preparing displays, advertising and otherwise promoting sales; and delivering goods to

buyers if the seller has agreed to pay the cost of delivery

General and administrative expenses – include expenses for accounting, personnel,

credit checking, collections and any other expenses that apply to overall operations.

, Operating income is the income from a company’s main business.

Operating income – gross margin – operating expenses.

Other revenues and expenses are not related to a company’s operating activities.

(revenues from investment; dividends and interest on stocks, bonds, and savings

account; interest expense and other expenses that result from borrowing money.)

NET income Gross margin – operating expenses +/- other revenues and expenses

Taxes: - interest earned: + interest paid: -

Ratio’s

Ratio’s use the components of classified financial statements to reflect how well a firm

has performed in term of maintaining liquidity and achieving profitability.

Liquidity

Working capital: the amount by which current assets exceed current liabilities

Working capital = current assets - current liabilities

Current ratio: ratio of current assets to current liabilities

Current ratio = current assets / current liabilities

Liquidity means having enough money on hand to pay bills when they are due and to

take care of unexpected needs for cash.

To determine whether a current ratio is good or bad, it must be compared with ratios for

earlier years and with similar measures for companies in the same industry.

Profitability

Profit margin: percentage of each sales dollar that results in NET income

Profit margin = NET income / NET sales

Asset turnover: ratio of sales dollars to assets

Asset turnover = NET sales / average total assets (av. Tot. assets = assets

beginning + assets ending / 2)

Return on assets: percentage of each dollar in assets resulting in NET income, thereby

combining the profit margin and the asset turnover

Return on assets = NET income / average total assets

Return on assets = profit margin X asset turnover

Debt to equity ratio: proportion of a company’s assets that is financed by creditors to

the proportion that is financed by the owner

Debt to equity ratio = total liabilities / owner’s equity

Return on equity: percentage of each dollar in owner’s equity resulting in NET income

Return on equity = NET income / average owner’s equity (av. OE = OE beginning +

OE ending / 2)

Profitability is the ability to earn a satisfactory income.

A company with a high asset turnover uses its assets more productively than one with a

low asset turnover.

Voordelen van het kopen van samenvattingen bij Stuvia op een rij:

Verzekerd van kwaliteit door reviews

Stuvia-klanten hebben meer dan 700.000 samenvattingen beoordeeld. Zo weet je zeker dat je de beste documenten koopt!

Snel en makkelijk kopen

Je betaalt supersnel en eenmalig met iDeal, creditcard of Stuvia-tegoed voor de samenvatting. Zonder lidmaatschap.

Focus op de essentie

Samenvattingen worden geschreven voor en door anderen. Daarom zijn de samenvattingen altijd betrouwbaar en actueel. Zo kom je snel tot de kern!

Veelgestelde vragen

Wat krijg ik als ik dit document koop?

Je krijgt een PDF, die direct beschikbaar is na je aankoop. Het gekochte document is altijd, overal en oneindig toegankelijk via je profiel.

Tevredenheidsgarantie: hoe werkt dat?

Onze tevredenheidsgarantie zorgt ervoor dat je altijd een studiedocument vindt dat goed bij je past. Je vult een formulier in en onze klantenservice regelt de rest.

Van wie koop ik deze samenvatting?

Stuvia is een marktplaats, je koop dit document dus niet van ons, maar van verkoper jschkx. Stuvia faciliteert de betaling aan de verkoper.

Zit ik meteen vast aan een abonnement?

Nee, je koopt alleen deze samenvatting voor €7,49. Je zit daarna nergens aan vast.