Samenvatting van de colleges van Institutional Investments van de master Business Administration - Financial Management aan de Vrije Universiteit. Naast de collegesheets is er ook een deel van literatuur samengevat.

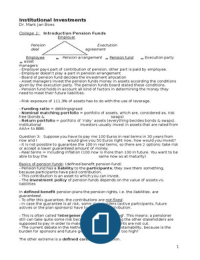

Employee Pension arrangement Pension fund Execution party

asset

managers

- Employer pays part of contribution of pension, other part is paid by employee.

- Employer doesn’t play a part in pension arrangement

- Board of pension fund decides the investment allocation

- Asset managers invest the pension funds money in assets according the conditions

given by the execution party. The pension funds board stated these conditions.

- Pension fund holds in account all kind of factors in determining the money they

need to meet their future liabilities.

- Risk exposure of 111,3% of assets has to do with the use of leverage.

- Funding ratio = dekkingsgraad

- Nominal matching portfolio = portfolio of assets, which are, considered as, risk

free (bonds & swaps)

- Return portfolio = portfolio of ‘risky’ assets (everything becides bonds & swaps).

Institutional investors usually invest in assets that are rated from

AAA+ to BBB.

Question 3: Suppose you have to pay me 100 Euros in real terms in 30 years from

now and I would give you 50 Euros right now, how would you invest?

- It is not possible to guarantee the 100 in real terms, so there are 2 options: take risk

or accept a lower guaranteed amount of money.

- Real terms = including inflation (100 now is more than 100 in future. You want to be

able to buy the same now as at maturity)

Basics of pension funds: (defined benefit pension fund)

- Pension fund has a liability to the participants; they owe them something,

because participants have paid contribution.

- This contribution is an asset to which you can invest.

- The investment policy of pension funds depends on the value of assets vs.

liabilities

In defined benefit pension plans the pension rights, i.e. the liabilities, are

guaranteed.

- To offer this guarantee, the contributions are not fixed.

- In case the guarantee is at risk, some stakeholders (active participants, future

actives or the plan sponsors) have to pay extra contribution.

- This is often called 'Intergenerational Risk Sharing'. This means: a pensioner

still can take quite some risk because if things go wrong the other stakeholders are

supposed to pay in order to make sure that pension rights are not cut.

- The current debate in the Netherlands is about the sustainability, because is the

burden for sponsors and future generations simply not too high?

The other extreme is a defined contribution system.

1

,- In this system the contributions are fixed and consequently, benefits are not

guaranteed.

- Investment risk is fully with the individual participant.

- Expectation for the future: combine the best of defined benefit and defined

contribution.

- Nowadays, ABN AMRO Pension Funds is a collective defined contribution scheme.

Participants invest collectively, contribution still varies with interest rates but benefits

are not guaranteed anymore.

Simplistically said, a defined benefit pension fund is:

a lot of participants (active participants, deferred (= slapers) participants,

pensioners)

a lot of liabilities towards the participants

a lot of payments to the pensioners (until they pass away)

a lot of contributions from the active participants (employees)

a lot of assets from present and past contributions plus investment gains /

losses

- From this simplistic representation you can already see that a pension fund is a

highly dynamic vehicle.

From the previous slides you can already ask a number of questions:

Do pension fund provide an explicit guarantee to their participants?

What is the ambition of the pension fund with respect to inflation

compensation?

Which risk level is acceptable in order to meet this ambition?

Who pays the contribution and how large should it be?

What is the optimal investment policy?

Nowadays it is popular in the pension fund community to summarize all these

questions in three major decision themes:

Ambition

Risks

Costs

- There is obviously a trade-off between these concepts, e.g., a higher ambition

comes with higher risk or with higher costs.

- The Boards of pension funds need to make the trade-off in such a way that the

interests of all stakeholders involved are served in a satisfying way.

Funding ratio (= dekkingsgraad)

- The nominal funding ratio is defined as the pension fund's assets over its nominal

liabilities:

FRt = At / Lt

* Where the liabilities are defined as:

Lt = ∑ T CFi

i=t (1 + Yt:i)^i-t

* In which y represents the discount rate observed at time t and CFi is the

expected payment at time i (= indexation)

What are the factors that drive the change in the nominal funding ratio?

FRt+1 = At x (1 + rAt:t+1) – Bt+1 + Ct+1

Lt x (1 + it ) x (1 + rLt:t+1) – Bt+1 + PRt+1 + Et+1

* Where rAt:t+1 is the return on the investment portfolio (return on assets)

* Bt+1 pension benefits that are paid by the pension fund to the pensioners

* Ct+1 contribution of the employer / employee that ow into the fund

* it is indexation

2

, * rLt:t+1 is the return on liabilities, i.e. change in pension fund liabilities due to

interest rate accrual and interest rate changes. Voorwaarden van berekeningen

veranderen.

* PRt+1 is present value of new pension rights

* Et+1 unknown factor that represents the possibility that people live longer and

it is the indexation given at time t: if the pension fund is sufficiently rich it will

increase all nominal rights with realised inflation (fully or partially). E is in this

case epsilom

Samengevat: Funding ratio =

Assets * (1 + return on assets) – pension benefits + contribution

Liabilities * (1 + indexation) * (1 + return on liabilities) – pension benefits + PV new

pension rights + unknown factor

- The liabilities can be interpreted as the present value of future obligations.

- The value of the assets is simply the value of the investment portfolio.

- Hence, the ratio of assets over the nominal liabilities says something about the

financial position of the pension fund.

- A ratio below 1 (or 100%) therefore says that the pension fund has insufficient

assets to cover its (future) obligations.

- The difficulty is that the pension fund doesn't need to pay the full amount of money

today. So, is a funding ratio below 1 really a problem?

From the formula for the nominal funding ratio, we can identify three possible policy

instruments:

Contribution policy: higher contributions lead to higher funding ratios

Indexation policy: no indexation leads to no increase in nominal liabilities

Investment policy: by taking more or less investment risk, funding ratio risk

can be steered

- These are usually the policy parameters in a so-called Asset and Liability

Management study.

- The policy instruments can be utilized (=gebruikt) to make the trade-off between

ambition, risks and costs.

Development funding ratios of three large pension funds:

- It turned out that pension funds took to much risk so when the crisis hit funding

ratio dropped.

The real funding ratio differs from the nominal funding ratio in the sense that future

expected cash- flows are corrected for (break-even) inflation:

FRrt = At / Lt

* Where the real liabilities are defined as:

Lrt = ∑ T CFi x (1 + πBEt:i)i-t

i=t (1 + yt:i)i-t

* Where y represents the discount rate observed at time t and πBE is the break-

even inflation that is observed in the inflation swap market.

* The difference between break-even inflation and expected inflation is the

inflation risk premium.

- For the exam it is not necessary to know the difference between expected inflation

and break-even inflation. It is sufficient to know how the real funding ratio is defined

and how it differs from the nominal ratio.

Pension funds continued

- Pension funds are interesting to know more about because more than 1,200 billion

euros is involved. This money is invested in all kinds of assets, because bank deposits

yields are too low.

3

, So what happens with the money? It is invested in a clever way. At least, that is the

aim.

- Some of the elements of the investment process:

Choosing a strategic investment policy (ALM study)

Choosing benchmarks for the asset classes

Determining risk budgets for individual portfolios

Implementing portfolio decisions, e.g. trading securities in the markets

Storage of physical assets

Performance measurement of individual portfolios

(Risk)-monitoring of balance sheet and contract parties

- A lot of these activities are outsourced by the Board of Trustees to asset managers,

custodians and performance specialists.

- Against fees, of course: on average Dutch pension funds pay 30-35bps for asset

management / consultancy plus 15bps transaction costs.

- Important examples in the Netherlands are APG and PGGM who advise and invest

for the largest Dutch pension schemes. But also traditional asset managers like

BlackRock, UBS Asset Management, PIMCO, ING Investment Management and Robeco

offer a lot of services to pension funds.

- Trading usually happens with banks as counterparty. So, revenues of large banks

like JPMorgan, RBS, Morgan Stanley, Goldman and Deutsche depend also on pension

fund trading.

Assume the following pension fund: (EXAMPLE)

the pension fund consists of 1 person

the pension fund promises to pay this person 100 Euros in 30 years from now

the pension fund has the knowledge that this person dies after he has received

the payment

the pension fund receives a contribution from the person

the ambition of the pension fund is to provide full indexation on top of the

promised 100 Euros

- In reality, we make a projection of the expected payments for all individual

participants.

- If the 30-years zero nominal interest rate is 3% then the present value of the

nominal obligation is: 100

(1 + 3%)^30 = 41.2

- If the 30-years annual expected inflation is 2% then the present value of the

ambition is:

100 x (1 + 2%)^30

(1 + 3%)^30 = 74.6

- This is the real liability value, i.e. the nominal liability value increased with expected

inflation (i.e. we assume that break-even inflation equals expected inflation). i.e. =

that is … (dat wil zeggen)

Let us consider two cases:

Case 1: the contribution equals 41.2 Euros

Case 2: the contribution equals 74.6 Euros

- Question: how would you invest in each of these cases?

Case 1: you could invest all the money in the matching portfolio: a portfolio that

matches the value of the liability perfectly (a single nominal zero coupon bond, in this

case). So the value goes from 41.2 to 100 in 30 years.

- The result is a stable nominal funding ratio

4

The benefits of buying summaries with Stuvia:

Guaranteed quality through customer reviews

Stuvia customers have reviewed more than 700,000 summaries. This how you know that you are buying the best documents.

Quick and easy check-out

You can quickly pay through EFT, credit card or Stuvia-credit for the summaries. There is no membership needed.

Focus on what matters

Your fellow students write the study notes themselves, which is why the documents are always reliable and up-to-date. This ensures you quickly get to the core!

Frequently asked questions

What do I get when I buy this document?

You get a PDF, available immediately after your purchase. The purchased document is accessible anytime, anywhere and indefinitely through your profile.

Satisfaction guarantee: how does it work?

Our satisfaction guarantee ensures that you always find a study document that suits you well. You fill out a form, and our customer service team takes care of the rest.

Who am I buying this summary from?

Stuvia is a marketplace, so you are not buying this document from us, but from seller BtB12. Stuvia facilitates payment to the seller.

Will I be stuck with a subscription?

No, you only buy this summary for R89,27. You're not tied to anything after your purchase.